Understanding car insurance exclusions is critical to avoiding financial pitfalls. These exclusions—specific scenarios your policy won’t cover—vary across liability, comprehensive, and collision policies. Common misconceptions, like assuming “full coverage” includes flood damage or mechanical breakdowns, can leave drivers exposed. In this guide, we’ll demystify auto insurance exclusions and car insurance exclusion clauses, empowering you to identify gaps and secure the right protection. Whether you’re in Dubai or Abu Dhabi, knowing these exclusions ensures you’re never caught off guard.

Understanding the Fine Print: What Are Car Insurance Exclusions?

Auto insurance exclusions are specific risks or scenarios explicitly removed from your policy’s coverage. Insurers define these in the “insuring agreement” to limit liability for high-risk or predictable events. For example:

- Named-Perils Policies: Only cover losses from events listed in the policy (e.g., theft, fire).

- All-Risk Policies: Cover everything except exclusions listed (e.g., comprehensive plans).

Why it matters: Misunderstanding these clauses can lead to claim denials. Exclusions protect insurers from fraud, intentional damage, or catastrophic losses like wars.

Car Insurance Exclusions in UAE

While many people are familiar with the basic types of coverage, there are significant car insurance exclusions that could leave you unprotected in various scenarios. These exclusions can vary between insurance providers and policies, making it imperative for car owners to familiarize themselves with the terms of their insurance contracts before hitting the road.

When evaluating auto insurance coverage limits, it’s crucial to recognize that not everything is included. For instance, damages incurred during racing or competitive events, vehicle theft due to negligence, and maintenance issues stemming from wear and tear are commonly excluded. Moreover, acts of nature, such as floods or earthquakes, may also not be covered depending on your policy. So, whether you’re navigating the bustling streets of Dubai or the serene landscapes of Abu Dhabi, knowing what is not covered in car insurance can help you avoid unpleasant surprises and ensure you’re prepared for all eventualities on the road.

Understanding what’s not covered by your policy is just as important as knowing what does full coverage car insurance cover. Comprehensive insurance provides broader protection, but it’s essential to know the specifics of what is included to ensure you have the right level of coverage.

Third-Party Car Insurance Coverage Exclusions

Understanding car insurance exclusions is essential for anyone with third-party car insurance. While this coverage is designed to protect you from claims made by others for damages or injuries you may cause, it’s important to be aware of the limitations. Knowing what’s left out of the policy can help you prepare for potential pitfalls and ensure you have the right type of coverage.

Accidents On Foreign Soil

If you’re driving abroad and end up in a collision, your third-party policy may not apply, leaving you financially responsible for any damages or injuries.

Damages Caused by Natural Disasters

Another significant aspect of what is not covered in car insurance under third-party policies involves damages resulting from natural disasters. Events like floods, earthquakes, or severe storms generally fall outside the realm of third-party liability. While your policy may shield you from claims made by other motorists, it won’t protect your vehicle from the devastation these disasters can bring. If you live in a disaster-prone area, it might be prudent to explore comprehensive or additional coverage options.

War-Time Damages

Third-party car insurance typically does not provide coverage for damages or liabilities incurred during war or armed conflict. If your vehicle is impacted by such events, you may find that seeking reimbursement from your insurer is not an option.

Personal Injury Protection (PIP) Exclusions

Under this type of insurance, coverage for injuries sustained by the insured driver or passengers in their vehicle is typically not included. If you or your passengers are injured in an accident where you are at fault, your third-party policy will not cover medical expenses, lost wages, or other related costs. This exclusion represents a key point regarding what is not covered in car insurance related to personal injuries. To address this gap, individuals should consider additional coverage options, such as comprehensive insurance or personal accident insurance, to ensure adequate protection in the event of an accident.

While PIP covers medical costs after accidents, key exclusions include:

- Injuries to the Insured: If you cause the accident, your own injuries may not be covered.

- Household Drivers: Regular drivers excluded in your policy (e.g., unlisted family members).

- Work-Related Incidents: Injuries during commercial deliveries fall under workers’ compensation, not PIP.

Example: A rideshare driver injured on duty must claim through workers’ comp, not auto insurance.

Comprehensive Car Insurance Coverage Exclusions

Comprehensive car insurance is designed to provide extensive coverage for a wide variety of risks, yet even this seemingly all-encompassing policy has its car insurance exclusions. Understanding what is not covered in comprehensive car insurance is crucial for ensuring you are adequately protected. Familiarizing yourself with these exclusions can save you from unexpected financial burdens down the line.

Off-Road Driving

If you take your vehicle on unpaved roads or engage in off-roading activities, you may find that the damages resulting from these adventures are not covered. To ensure you’re protected, consider discussing specific activities with your insurer or exploring specialized coverage.

Mechanical Electrical Breakdown

While comprehensive insurance offers protection against theft, vandalism, and certain accidents, it typically does not cover damages resulting from mechanical failures. Wear and tear on vehicle parts or issues stemming from regular maintenance are often excluded. Therefore, considering a separate warranty or mechanical breakdown insurance might be a wise move to safeguard against potential repair costs.

When reviewing car insurance, it’s essential to understand what’s not covered. For electric vehicles, electric car insurance provides coverage that includes specific risks and protections unique to EVs. Make sure you choose the right policy to avoid unexpected exclusions and ensure your electric car is fully protected.

Violating Certain Laws

If you’re involved in an accident while breaking the law—such as driving under the influence or without a valid license—your policy may not provide coverage for damages or liabilities.

Unlicensed Driver

Driving with an unlicensed driver at the wheel is another scenario that can leave you without coverage under a comprehensive policy. If you’re involved in an accident while someone without a valid driver’s license is driving your vehicle, the claim could be denied outright.

Intentional Damage

This is one of the key car insurance exclusions, meaning you cannot claim for damage you purposely caused. This means that if you deliberately damage your vehicle or cause harm to someone else’s property out of malice or intent, you will not be able to file a claim for car insurance and those damages. This exclusion protects insurers from fraudulent claims and highlights the importance of honest and responsible behavior while operating a vehicle.

Use of Vehicle for Commercial Purposes

Coverage typically does not apply if the vehicle is used for commercial activities without proper endorsement. This reinforces the need for drivers to be aware of auto insurance coverage limits regarding commercial use to avoid claim denials. This can include using a personal vehicle for ride-sharing services, deliveries, or other business-related tasks.

Racing or Speed Trials

This is another instance of what is not covered in car insurance, as engaging in these high-risk activities poses significant dangers. Engaging in high-speed competitions poses significant risks not only to the driver but also to others on the road. Therefore, insurance providers exclude these scenarios to mitigate potential losses resulting from such high-risk activities. If you’re interested in participating in racing, you may need to explore specialized insurance options designed for motorsport activities.

Unsecured Infant/Child Safety Seats

Coverage may be denied if children are not properly secured in safety seats. This is a critical point of car insurance exclusions, emphasizing the importance of passenger safety and compliance with regulations.

Special Auto Insurance Exclusions

- Excluded Drivers: Claims denied if a driver explicitly named in your “excluded drivers” list uses your car.

- Geographic Limits: Damages abroad (e.g., Oman road trips) often void coverage without travel endorsements.

- Government Seizures: Confiscation during repossession or by authorities is never covered.

- Rideshare Gaps: Personal policies exclude Uber/Delivery work—require commercial endorsements.

How Coverage Gaps Cost Drivers

- Undeclared Modifications: Adding a tow bar or custom rims without endorsement → $5k claim denied.

- Personal Belongings: Stolen laptops from your car excluded—requires renters/home insurance.

- Policy Limit Shortfalls: Total loss of a $30k car with $20k coverage → $10k out-of-pocket.

- Rental Car Coverage: Not automatic; add-ons cost ~$1/day but save thousands in accidents.

How to Avoid Car Insurance Exclusions Traps

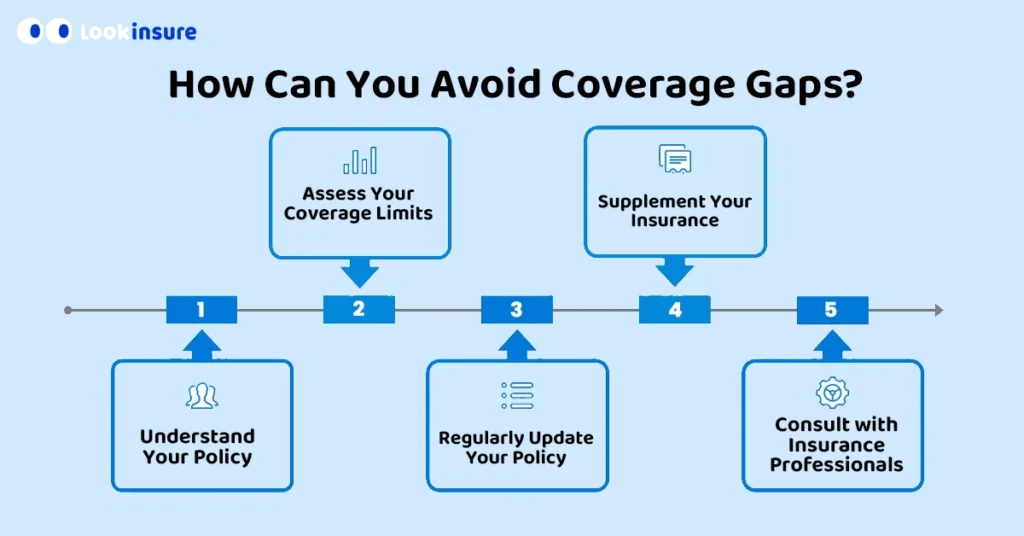

A coverage gap refers to a situation where you lack sufficient insurance protection for specific risks, leaving you financially vulnerable in the event of an accident or loss. It often occurs when policy limits are too low, when specific situations are not adequately covered, or when exclusions are not fully understood. To avoid these gaps and ensure comprehensive protection, consider the following strategies.

Decoding Car Insurance Exclusion Clauses: Your Policy’s Fine Print

Car insurance exclusion clauses are contractual terms that explicitly remove specific risks, losses, or scenarios from your coverage. Insurers use these legally binding provisions to limit liability for high-cost, predictable, or preventable events. Understanding these clauses is non-negotiable—ignoring them can void claims.

How Car Insurance Exclusion Clauses Work

- Scholarly Definition (per Cornell Law School):“Exclusion clauses modify the insurer’s promise to indemnify by carving out exceptions to coverage.”

- Legal Language in Policies:

- Broad Car Insurance Exclusions: Blanket denials (e.g., “No coverage for illegal acts”).

- Specific Auto Insurance Exclusions: Narrow scenarios (e.g., “Flood damage excluded unless Addendum X is purchased”).

Top 3 Types of Car Insurance Exclusion Clauses

| Clause Type | Purpose | Real-World Example |

|---|---|---|

| Absolute Exclusions | Permanently removes coverage | “War, nuclear hazards, or government confiscation” |

| Conditional Exclusions | Coverage void if rules broken | “Denial for DUI or unlicensed driving” |

| Partial Exclusions | Limits payout scope | “$1,000 cap for stolen personal items” |

Why Insurers Use Them

- Risk Mitigation: Avoid covering catastrophic losses (e.g., floods, wars).

- Fraud Prevention: Exclude intentional damage or illegal acts.

- Cost Control: Eliminate predictable claims (e.g., wear-and-tear).

Controversial Clauses & Legal Loopholes

- The “Racing Exclusion” Trap:Even non-competitive track days may trigger this clause (per NAIC).

- “Household Driver” Ambiguity:Excluded family members void coverage even with permission (Vanderbilt Law Review).

- Jurisdiction Limits:UAE policies often exclude accidents in Oman/Saudi without a travel endorsement.

Key Takeaway

Car insurance exclusion clauses are not boilerplate—they’re negotiable. Demand written clarification, use endorsements to override them, and contest vague language. As the contra proferentem rule states: “Ambiguous clauses are interpreted AGAINST the insurer.”

Assess Your Coverage Limits

Regularly evaluate your auto insurance coverage limits to ensure they are sufficient for your current vehicle and financial situation. Adjusting these limits proactively can help protect you from significant out-of-pocket expenses in a claim.

Regularly Update Your Policy

Life changes, such as relocating or changing how you use your vehicle, may necessitate updates to your policy.

Supplement Your Insurance

Consider purchasing additional coverage options, like comprehensive or personal injury protection, to address any specific exclusions in your current policy. This extra coverage can fill gaps and provide enhanced protection against unforeseen events.

Consult with Insurance Professionals

Engage with an insurance agent or Lookinsure professionals who can help you navigate complex policy details and identify any potential gaps.

How to Avoid Third-Party Car Insurance Coverage Gaps

Begin by reviewing the specific car insurance exclusions related to personal injury and property damage, as these can significantly impact your coverage. Additionally, regularly check if your policy meets the legal requirements and consider handling any special driving situations, such as using your vehicle for commercial activities.

How to Avoid Comprehensive Car Insurance Coverage Gaps

Start by evaluating the auto insurance coverage limits to ensure they are adequate for your vehicle’s value and your lifestyle. Pay attention to the specific what is not covered in car insurance, especially regarding natural disasters, mechanical failures, and modifications to your vehicle. Periodic reviews and updates will help maintain comprehensive protection and close any potential gaps in coverage.

Stay Protected: Close Your Coverage Gaps

Car Insurance Exclusions don’t have to leave you vulnerable. By proactively reviewing your policy, adding endorsements for high-risk scenarios, and consulting experts, you can transform exclusions into actionable safeguards. Remember: understanding auto insurance exclusions is your first step toward peace of mind on the road. Regularly update your coverage, ask questions, and drive confidently—knowing you’ve turned potential pitfalls into solid protection.

Frequently Answered Questions

1: What does comprehensive car insurance not cover?

Comprehensive car insurance usually does not cover damage due to wear and tear, mechanical failures, or routine maintenance. Additionally, it typically excludes intentional damage, theft of personal items inside the car, and any claims while using the vehicle for illegal activities.

2: What damage does car insurance not cover?

Car insurance generally does not cover damage resulting from driving under the influence, racing, or using the vehicle for commercial purposes without proper endorsement. It also excludes damages from acts of war or nuclear hazards.

3: Does car insurance cover natural disasters in the UAE?

Yes, comprehensive car insurance often covers damage resulting from natural disasters, such as floods or storms, in the UAE. However, coverage specifics can vary by policy, so it’s essential to verify provisions with your insurer.

4: Is personal item theft covered?

No, personal items inside your car, like electronics or clothing, are not covered by your auto insurance. For theft of personal belongings, you should rely on your homeowner’s or renter’s insurance policies, which typically provide broader coverage for personal property.

5: What if an excluded driver crashes my car?

Claims involving drivers who are explicitly excluded from your policy are typically denied. Make sure all regular drivers are listed on your policy to avoid coverage disputes if an incident occurs with an unlisted driver.

Comments (0)

Leave a comment