Here’s the truth: many car owners in the UAE think they know what their policy covers, when in reality, they only know a small part of it. Look, It’s not your fault it’s them! Honestly insurers aren’t exactly eager to highlight every exclusion or cost that hides in the small print. There are hidden costs of car insurance in UAE that only come to light when something goes wrong!

This article will break that wall of confusion for you. You’ll learn about the types of auto coverage in UAE, what insurance companies often don’t disclose (like those sneaky add-on fees and silent policy limits), and the factors secretly affecting your premium prices. We’ll also walk through how to spot common car insurance scams and share insider tips to help you get better, fairer quotes.

Types of Auto Insurance in UAE

When it comes to auto coverage in UAE, there are two main types you can choose from. The first is what the law demands, and the second is what actually protects your own car when things go wrong. Here’s how they differ:

Third-Party Liability Insurance

This is the most basic and legally required form of auto coverage in UAE. It covers injuries or property damage you cause to other people in an accident, but not your own car. So if your bumper is smashed or your headlights are gone, you’ll have to pay out of pocket.

Third-party insurance doesn’t include protection against theft, fire, or natural disasters, which makes it a practical but limited option. It’s often chosen for older or low-value cars where full protection might not make financial sense.

Comprehensive Auto Coverage

Comprehensive plans go several steps further. They protect both your car and third-party damages up to AED 1 million in most policies. This type of insurance includes coverage for theft, fire, vandalism, and natural disasters like floods or sandstorms (which are more common in the UAE than many realize).

Comprehensive policies can also be customized with add-ons such as agency repairs, roadside assistance, or personal accident cover. They cost more, but for newer or luxury vehicles, the extra protection is usually worth it. Since they cover much more than the average TPL policies, comprehensive plans are were you are likely to see most of the hidden costs of car insurance in UAE.

Quick Comparison: How Coverage Limits Differ

| Coverage Type | Property Damage Cap | Passenger Injury Limit | Covers Your Own Car? | Common Exclusions |

| Third-Party Insurance | AED 250K–500K | ~AED 200K per passenger | No | Theft, fire, natural disasters, your own damage |

| Comprehensive Insurance | Up to AED 1 million | Customizable (AED 200K–500K+) | Yes | Wear and tear, mechanical failure, unapproved mods |

Which One Is Mandatory by Law?

According to the laws on auto coverage in the UAE, every vehicle owner to have at least third-party insurance. Without it, the RTA won’t even let you register your car. However, if your car is financed through a bank loan, you’ll most likely need comprehensive coverage. That way the bank feels that their asset is adequately protected and so feel more inclined to loan the car owner the money.

For example, insuring a Honda City with third-party coverage might cost around AED 350–400 a year, while a comprehensive policy could range from AED 1,000 to 1,500 depending on the provider and add-ons. The price gap is noticeable, but so is the level of protection.

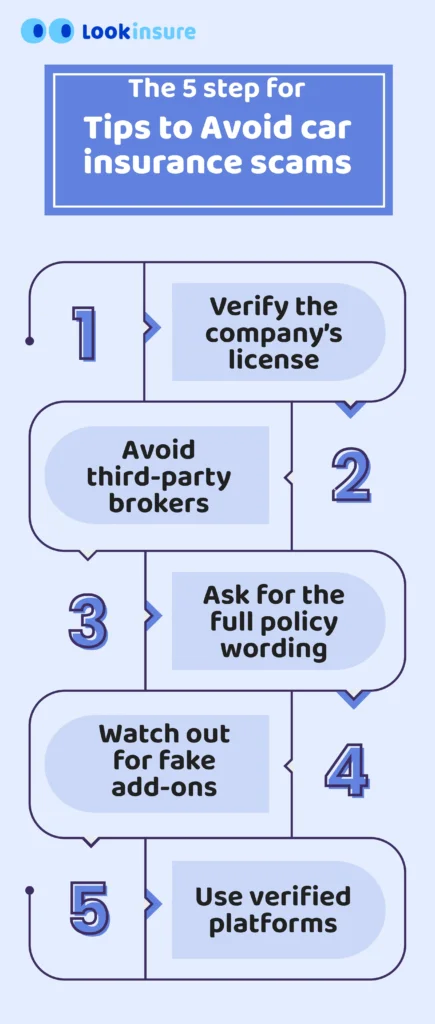

Tips to Avoid Common car insurance scams

When you hear about common car insurance scams you probably think about car owners trying to scam insurance companies by staging accidents. But sometimes it can be the car owner who ends up being scammed. Here is how you can avoid such scams:

- Verify the company’s license through the UAE Central Bank website, they regulate all insurance providers.

- Avoid third-party brokers who promise unrealistically low prices. If a quote sounds too good to be true, it usually is.

- Ask for the full policy wording in writing, not just a summary. The fine print is where you can find out about hidden costs of car insurance in UAE.

- Watch out for fake add-ons some scammers sell “accident forgiveness” or “lifetime repair” plans that aren’t real products.

- Use verified platforms like Lookinsure or trusted UAE insurance portals instead of random social media ads.

Insurance Designs and Hidden Meanings

Here’s the part insurance companies rarely bring up: THE FINE PRINT. The shiny policy brochure talks about “peace of mind,” but the real details hide in pages you probably never read. Let’s break down what’s actually inside those terms and conditions, and how you can avoid falling into traps or common car insurance scams that still happen in the UAE.

Hidden Caps on Property Damage

Most drivers assume their policy will cover all accident costs, but third-party policies in the UAE often have hidden caps between AED 250,000 and 500,000. That sounds like a lot until you hit a luxury car worth millions. The gap between what your insurer pays and the actual repair bill? That’s on you.

Some insurers offer optional add-ons to extend this limit, but they rarely mention them upfront. Always ask directly about these coverage caps before signing anything.

Important Tip to Consider: Always ask your insurer if your third-party coverage includes optional upgrades to raise this limit. Some companies quietly offer an add-on for AED 100–200 per year that doubles your coverage cap, but they rarely bring it up unless you ask.

Interesting Fact to Know: Comprehensive plans, by comparison, usually include up to AED 1 million in third-party property damage as standard. So if you drive in high-traffic areas like Dubai Marina or Sheikh Zayed Road, the extra protection is worth every dirham.

Passenger Injury Limits and Exclusions

Many policies quietly limit payouts for passengers to around AED 200,000 per person. And here’s the tricky part : domestic workers, family members, or anyone in a carpool might not be covered under certain clauses.

Even more surprising, if you use your car for “business purposes” (say, informal ride-sharing or deliveries), your claim could be rejected entirely. Always check whether “passenger coverage” applies to everyone who regularly rides with you.

Important Tip to consider: If you regularly drive with family or staff, ask about “personal accident cover for passengers.” It’s usually an affordable add-on for auto coverage in UAE, but many drivers skip it because it’s not mentioned during signup.

Interesting Fact to know: Some comprehensive policies already include basic passenger protection, but the amount is low unless you increase it manually. Always check how many passengers are actually covered and at what payout limit.

Why Your Own Car May Not Be Fully Covered

Even with comprehensive auto coverage in UAE, you might not get the full amount you expect after a claim. Insurance companies factor in depreciation, meaning every year, your car’s parts lose value. Items like batteries, tires, and electronics are especially affected.

Deductibles (the amount you pay out of pocket before insurance kicks in) typically range from AED 350 to 1,500. Add to that the fact that normal wear and tear isn’t covered, and you’ll see how fast small issues can add up.

Important Tip to consider: To reduce depreciation-related losses, check if your insurer offers “agency repair” for the first 3–5 years of your car’s life. Agency workshops use genuine parts and may preserve your car’s resale value.

Interesting Fact to know: Some premium insurers offer a “new-for-old” replacement policy for cars under one year old. That means if, god forbid, your car is totaled in the first year, they’ll replace it with a brand-new one, not just pay the depreciated value.

Add-Ons That Can Make or Break Your Policy

When you’re comparing auto coverage in UAE, the base price might look appealing but what really shapes the value of your policy are the add-ons. These extras are where you’ll encounter most of the hidden costs of car insurance in UAE which can save you a fortune when something goes wrong or leave you stranded if you skip them without understanding the trade-off. Let’s go through the most important ones you should know before hitting “buy.”

Agency vs Non-Agency Repairs

This is one of the most common decisions drivers face when it comes to auto coverage in UAE. Agency repair means your car is fixed at the official dealership using genuine parts, which keeps your warranty intact and your service record clean. Non-agency repair, on the other hand, sends your vehicle to insurer-approved garages, cheaper, usually faster, but sometimes not as precise.

For brand-new or luxury cars, agency repair is usually worth the higher price. For older cars, non-agency is the budget-friendly route.

Car Rental and Roadside Assistance

Rental car coverage makes sure you’re not left stranded when your car is in the shop. It gives you a replacement car for a few days. It’s totally perfect if you rely on your vehicle daily.

If you have ever been unlucky enough to get a flat in the middle of a highway, you probably know well how towing companies take advantage of you in such situation by charging you as much as they like. This is where such an add-on comes into play. Roadside assistance is another small but smart add-on that provides towing, jump-starts, and help with flat tires. Think of it as your trusty sidekick for those sweltering days, turning a tricky moment into a quick, smooth recovery.

GCC Coverage and Off-Road Protection

If you enjoy road trips to Oman or Saudi Arabia, GCC coverage extends your insurance across borders. It’s surprisingly affordable and can save you from huge headaches abroad.

Meanwhile, off-road protection is a must for SUV and 4WD owners who love desert drives. Just keep in mind: “off-road” doesn’t always mean “dune racing”. Check your policy to see what’s actually covered so that you don’t face any of the hidden costs of car insurance in UAE.

No-Claim Bonus and Protection

A No-Claim Bonus (NCB) rewards you for safe driving with 10–20% discounts after each claim-free year. The good news? You can take that bonus with you when switching insurers or buying a new car.

There’s also an optional “NCB Protection” add-on: it keeps your discount intact even if you file a small claim. So you don’t have to sacrifice your reward for a minor hiccup.

Add-On Comparison Table

This little snapshot below helps you compare options at a glance and choose what fits your needs without any guesswork. Remember that Choosing the right mix of add-ons doesn’t just personalize your plan. Actually it shields you from the hidden costs of car insurance in UAE that so many drivers discover too late.

| Add-On | What It Does | Who It’s Best For | Typical Extra Cost (Per Year) |

| Agency Repair | Repairs at dealer workshops using genuine parts | New/luxury car owners | AED 300–600 |

| Non-Agency Repair | Repairs at insurer-approved garages | Older car owners | Included or AED 0–100 |

| Car Rental | Temporary replacement vehicle after an accident | Daily commuters | AED 150–300 |

| Roadside Assistance | Towing, jump-start, flat tire, emergency fuel | All drivers | AED 100–200 |

| GCC Coverage | Cross-border protection in GCC countries | Frequent travelers | AED 150–400 |

| Off-Road Protection | Covers 4WD use off paved roads | Adventure/4WD drivers | AED 250–500 |

| No-Claim Bonus (NCB) | Discounts for claim-free driving | All safe drivers | Included |

| NCB Protection Add-On | Keeps your NCB after one minor claim | High-value car owners | AED 100–150 |

Key Takeaways

- Auto coverage in UAE comes in two main types : third-party liability (the legal minimum) and comprehensive insurance (for broader protection). Third-party is cheaper but won’t cover damage to your own car.

- The hidden cost of car insurance in UAE in many policies comes in the shape of hidden caps on property damage (usually AED 250K–500K) and passenger injury limits, so you have to ask about these before you buy.

- Even comprehensive insurance has limits such as depreciation, deductibles, and exclusions for wear and tear can reduce your payout.

- Watch out for the hidden costs of car insurance in UAE, like small add-on fees, claim-handling charges, or quietly applied premium hikes after renewals.

- Smart add-ons (like roadside assistance, rental car cover, and NCB protection) can turn a basic policy into a real piece of cake without breaking the bank.

- Always verify your insurer’s registration through the UAE Central Bank to avoid common car insurance scams or fake brokers.

- Don’t just compare prices. Compare what’s actually covered. The cheapest policy isn’t always the best deal if it leaves you unprotected in a real accident.

- And in overall: take a little time to read the fine print, ask the awkward questions, and tailor your plan. That’s how you protect both your car and your wallet from surprises later.

Conclusion

Most people treat car insurance like a gym membership. They sign up, pay every month, and hope they’ll never actually need it. But in the UAE, where one wrong turn can cost thousands, understanding your policy is not just smart, it’s survival.

The UAE insurance market is full of polished ads and tempting “cheap” offers, but the real cost often hides in the fine print. Quiet fees, sneaky exclusions, and claims that vanish into “policy terms.” Outrunning those traps isn’t about luck; it’s about knowing where they hide.

So before you hit renew, take ten minutes to read between the lines, question every add-on, and double-check who you’re really buying from so you don’t end up as victim of common car insurance scams.

Frequently Answered Questions

1. What are the hidden costs of car insurance in UAE?

Hidden costs include administrative fees, excess charges, depreciation deductions, add-ons and higher renewal premiums not shown in initial quotes.

2. Why is comprehensive insurance more expensive than third-party in UAE?

Comprehensive insurance covers both your car and third-party damages, plus theft, fire, and natural disasters, making it more extensive and costly.

3. What are the most common car insurance scams to avoid?

Watch out for fake brokers, unlicensed insurers, and unrealistic low-price offers. Always verify the provider with the UAE Central Bank.

4. How do auto coverage limits in UAE really work?

Third-party coverage usually caps at AED 250K–500K, while comprehensive policies go up to AED 1 million. Any excess amount is paid by the driver.

5. Are add-ons like roadside assistance and GCC coverage worth it?

It depends on your driving habit. If you spend a lot of time on the road or travel to other countries a lot, then yes, they are a good option to add to your policy.

6. How can I reduce my premium costs without losing coverage?

Compare insurers, keep a clean driving record, use your No-Claim Bonus, remove unnecessary add-ons, and opt for higher deductibles.

Comments (0)

Leave a comment