Planning to add a driver to your car insurance? Whether for family sharing or frequent borrowing, securing additional driver cover is crucial. This guide reveals exactly how to add a driver to insurance in the UAE covering legal requirements, cost factors, and a streamlined 4-step process to update your policy correctly.

What Is Additional Driver Cover?

Additional driver cover is a policy endorsement that formally authorizes specific individuals (beyond the primary policyholder) to drive your vehicle. Unlike the primary driver (typically the main user), named drivers are assessed for their risk profile, ensuring accurate premium calculations and legal compliance. This distinction is critical:

- Named drivers (e.g., spouse, children) are permanently listed on the policy, with their driving history directly impacting premiums.

- Permissive drivers (occasional users like friends) may be covered under comprehensive policies without formal addition, but claims involving them face stricter scrutiny and potential denial if usage is frequent.

Failing to name regular drivers risks “fronting” – a fraud where a high-risk driver (e.g., a teen) poses as low-risk primary, voiding claims and incurring legal penalties

Fronting

The reason this is necessary in such cases is to avoid fronting, a form of insurance fraud where a low-risk driver acts as the policyholder for a less experienced, high-risk driver to secure a lower premium price. To prevent these cases, insurance companies are more vigilant with claims involving another driver. Learning about different types of car insurance can help you understand how to avoid complications like fronting.

When Should You Add a Driver to Insurance?

Add drivers to your policy in these scenarios to ensure compliance and coverage:

- Household members: Spouses, children (with valid licenses), parents, or roommates using the vehicle weekly.

- Employees or caregivers: Domestic helpers, nannies, or chauffeurs driving for errands or family duties.

- Long-term car-sharing or rentals: Co-owners or long-term renters in formal arrangements (e.g., 6+ months).

Exception: Occasional users (e.g., friends borrowing twice yearly) fall under “permissive use” in comprehensive policies but require explicit owner permission.

In such cases, it is better to spend some extra money on the named driver add-on to avoid potential issues, especially if you’re considering policies like comprehensive vs third party insurance.

How to Add a Driver to Insurance – Step-by-Step

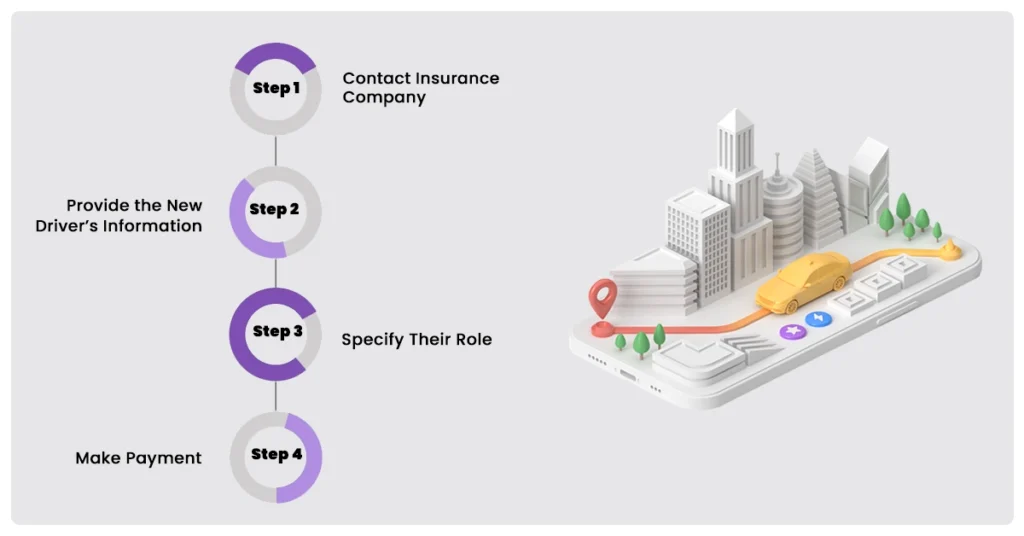

Adding a new driver to your insurance policy is a quite simple procedure and can be managed in 4 easy steps:

Step 1: Contact the Insurance Company

First, you must contact your insurance provider—whether online, via phone, or in person by visiting their nearest branch. If you’re considering switching policies, exploring changing car insurance may also be an option.

Step 2: Provide the New Driver’s Details

After letting them know the purpose of your visit they will naturally want to have access to the information of your additional driver. This information which includes their driving history is pivotal in determining their risk level which in turn affects the cost of your premium.

Step 3: Specify Their Role

When adding a driver to car insurance, you must specify who will be the primary and secondary driver. This designation is critical for assessing risk and setting the premium. For families with multiple vehicles, multi car insurance might be worth exploring to manage multiple drivers efficiently.

It’s essential that both drivers adhere to their assigned roles, as any breach of the agreement could lead to claim denial. Ensure the person using the car more frequently is listed as the primary driver

Step 4: Pay the Additional Driver Cover Fee

After the insurance agent calculates your premium based on the new driver’s details, you must make the payment. Once the payment is processed, the new driver will officially be added to your policy document. Insurer issues revised policy reflecting the added driver within 24–48 hours.

For short-term needs, temporary car insurance could be an alternative to adding a permanent named driver, especially if someone borrows your car infrequently. By following these steps and selecting the appropriate coverage, you can effectively protect yourself and the additional driver.

Who Qualifies as an Additional Driver?

Additional driver cover eligibility hinges on:

- Valid licensing: UAE residents require a local license; tourists need an international driving permit + passport/visa copy.

- Age restrictions: Most insurers mandate drivers be 25+; exceptions exist for spouses aged 21+.

- Clean record: Accidents or violations within 2 years may disqualify high-risk drivers

How Much to Add a Driver to Your Car Insurance?

The cost of adding a driver to car insurance in the UAE may vary between AED 300 to AED 1000 depending on some decisive factors such as the following:

- New Driver’s Age: Younger drivers with little driving experience and senior citizens usually tend to increase the cost of the premiums.

- Driver’s Record: if the new driver has a clean driving history that conveys their low level of risk, it will decrease the price.

- Car Value: the more valuable the car is, the more expensive it will be to insure it. Adding a new driver to your policy can be also pricier when you drive a luxury car.

Cost & Premium Impact of Additional Driver Insurance

Adding a driver variably affects premiums:

- Premium adjustments: Based on the driver’s risk profile. Low-risk drivers (clean record, age 30–50) may reduce premiums by up to 18%, while young (<25) or inexperienced drivers increase costs.

- Fees: Insurers charge AED 300–1,000 as a one-time processing fee, scaled to vehicle value (luxury cars incur higher fees).

- Long-term impact: Adding a low-risk secondary driver can distribute risk, potentially lowering annual renewals

Coverage Details & Legal Compliance

- Coverage scope: Named drivers receive identical benefits as the policyholder under comprehensive plans (e.g., accident liability, theft).

- Fraud prevention: “Fronting” (misrepresenting primary drivers) is illegal and voids claims – UAE insurers investigate accidents involving unlisted regular drivers rigorously.

- Claim denial risk: Insurers may reject claims if frequent drivers are unnamed, citing policy breaches

Named Drivers vs Permissive Use

| Aspect | Named Driver | Permissive Use |

|---|---|---|

| Definition | Formally added to policy; risk-assessed | Occasional borrower with verbal permission |

| Coverage Status | Fully covered; claims rarely disputed | Covered only under comprehensive policies |

| Risk Profile | Insurer evaluates driving history | Not evaluated; owner assumes liability |

| Ideal For | Regular users (e.g., spouse, teen drivers) | Infrequent borrowers (e.g., friends 1–2x/year) |

| Legal Risk | Low; compliant with UAE regulations | High; frequent use may trigger “fronting” probes |

Buy Additional Driver Cover Online

If you are looking to update your car insurance, an online comparison tool provides an all-in-one platform to find additional driver insurance quotes, upload documents, and register insurance in the fastest way possible. These KYC systems are streamlined for proficiency, allowing insurance buyers to find personalized quotes quickly.

Secure Your Coverage Today

Adding additional driver cover is a non-negotiable safeguard for UAE vehicle owners. Failing to authorize regular drivers risks formally claim denials, “fronting” fraud accusations (fines up to AED 10,000), and policy cancellation. Updating your policy takes under 48 hours but guarantees lifelong peace of mind. Use a comparison tool today to add a driver to your car insurance legally and lock in compliant UAE coverage! Protect yourself by understanding these critical takeaways:

- Definition & Purpose: Additional driver insurance formally authorizes frequent users beyond the primary policyholder, preventing illegal fronting practices.

- When to Add: Essential for household members (spouses/children), employees (nannies/drivers), or long-term users; excludes occasional borrowers.

- Qualification Rules: Candidates must have valid UAE/international licenses, a minimum age (typically 25+), and clean driving records.

- Process: Complete five steps: contact insurer → provide driver details → specify primary/secondary role → pay fee (AED 300–1,000) → receive updated policy.

- Cost Impact: Premiums adjust based on risk—may decrease 18% with low-risk drivers or surge for young/inexperienced users.

- Legal Compliance: Named drivers receive full coverage; undisclosed regular users void claims and incur penalties.

- Coverage Clarity: You need to add a driver to insurance policies for weekly users; permissive use applies only to occasional borrowing.

Frequently Answered Questions

1. How can I add a secondary driver to my car insurance?

Adding a secondary driver to your car insurance is quite a simple procedure and can be done by contacting your insurance company and providing them with the information of your new driver, including their driver history which will be used to determine the cost of your premium based on the new driver’s risk level.

2. Can my wife drive my car in the UAE?

Anyone with verbal or written permission from the owner can use their car and be covered in case of accidents. However, if someone else besides you uses your vehicle regularly, it is better to officially add them to your policy to prevent issues with filing claims in the future.

3. Can I transfer car insurance to another person in the UAE?

You can transfer Car insurance in the UAE depending on your insurance company’s policies. For more information contact your insurance provider.

4. Can anyone drive an insured car in Dubai?

Anyone with permission from the owner can drive a car and be covered by insurance in the event of an accident. However regular use of someone else’s car might bring about complications in claim processing.

5. Can I drive a friend’s car in the UAE with an international license?

NO, visitors and tourists with an international driving license are only allowed to drive rentals in the UAE. However, first-degree relatives are allowed to drive your car.

6. Does comprehensive insurance cover other drivers?

Yes, they usually do. But it is always better check your policy details before letting someone else drive your car.

Comments (0)

Leave a comment